- April 14, 2026

Double materiality in sustainability reporting

Following on from her blog article published earlier this year about sustainability reporting, our Senior Consultant Anna Rinaldi has now shared with us her views also about double materiality.

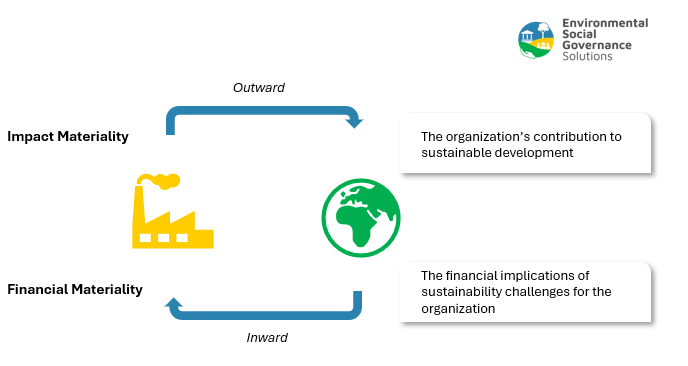

Double materiality is a key concept in sustainability reporting, recognising that sustainability issues are relevant from two distinct perspectives: impact materiality and financial materiality.

- Impact materiality focuses on how an organisation’s activities affect the environment, economy and people, both positively and negatively, over the short and long term. This outward-looking perspective considers impacts beyond the organisation itself and is relevant to stakeholders such as customers, employees, investors and communities.

- Financial materiality, on the other hand, takes an inward-looking perspective. It assesses how sustainability-related challenges and risks affect the organisation’s financial performance and long-term value, primarily for investors and capital providers.

Importance of this dual approach

Benefits of the double materiality approach include:

- Stakeholders: Provides relevant information for a wide range of stakeholders fostering stronger engagement. Improves transparency and trust by considering multiple stakeholder perspectives.

- Risk management: Helps identify sustainability-related risks that may become financially material over time. Links impacts to future financial risks and opportunities, improving organisational resilience.

- Credibility: Demonstrates that the organisation recognises responsibilities beyond financial performance, reinforcing commitment to society and the environment.

Trends of double materiality

Double materiality reporting is increasingly becoming a standard practice as organisations seek to provide a comprehensive view of their sustainability efforts and the implications for long-term value creation. This approach reflects the growing recognition that financial performance and sustainability performance are deeply interconnected, with sustainability performance increasingly affecting financial outcomes.

In practice, many organisations may be using established frameworks to guide their reporting e.g. the GRI Standards for impact reporting and the TCFD or TNFD frameworks for sustainability-related financial reporting.

A clear trend we’ve seen is the integration of multiple perspectives, impact and financial, within a single report, rather than producing separate reports. This means that sustainability-related information and impact-related information are presented together to provide a holistic and comprehensive view of an organisation’s performance, strategy and value creation, making it easier to communicate with a multi-stakeholder audience.

Leave a Comment