- July 10, 2026

Unpacking Scope 3: Category 15 – Investments

GHG Scope 3 Downstream activites | Category 15 – Investments

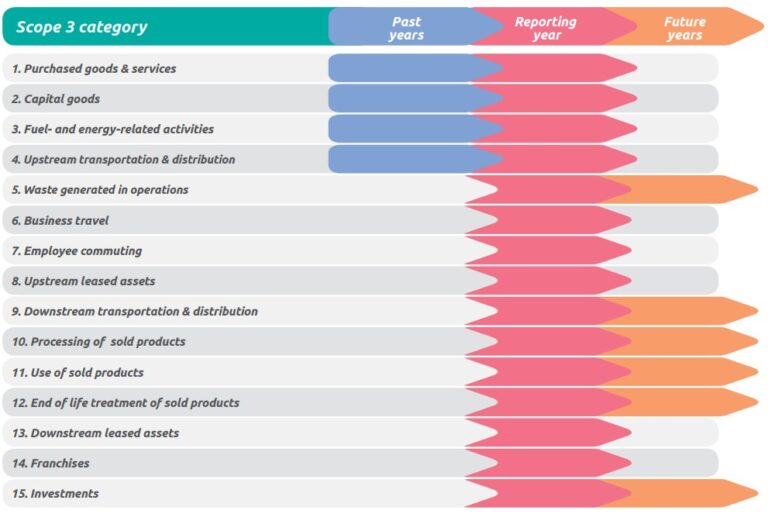

Introducing the last category of the “downstream” Scope 3 emissions, whose time boundary has NOT happended BEFORE the reporting period. Category 15 is also the last item of the historic categories included in the GHG Protocol publication “Corporate Value Chain (Scope 3) Accounting and Reporting Standard“, before the Greenhouse Gas Protocol underwent a Scope 3 standard revision, announced in March 2026 after this Carbon Clarity series curated by our colleague Rutuja Dongare was launched.

Understanding emissions linked to financed activities and capital allocation

For many organizations, particularly financial institutions, the most significant climate impact does not come from offices, travel, or purchased goods. It comes from where they allocate capital. Scope 3 Category 15 captures greenhouse gas (GHG) emissions associated with investments, loans, project financing and other financial activities.

Category 15 includes emissions from companies, projects or assets that the reporting organization invests in or finances. These emissions are often referred to as financed emissions.

This category is especially important for banks, asset managers, private equity firms, insurance companies, pension funds and corporations with equity stakes in joint ventures or subsidiaries not fully consolidated in Scope 1 and Scope 2.

What does this mean in practice?

If a bank provides financing to a coal-fired power plant, a portion of that plant’s emissions may be attributed to the bank.

If an investment firm owns shares in a cement manufacturing company, it may report emissions proportional to its ownership stake.

If a corporation holds minority investments in energy-intensive businesses that are not operationally controlled, those emissions may fall under Category 15.

In essence, this category applies when your capital enables economic activities that generate emissions.

Why Category 15 matters

For financial institutions, financed emissions can be many times larger than operational emissions. A bank’s office electricity use may be small compared to the emissions generated by its lending portfolio.

Category 15 is increasingly central to climate disclosure expectations. Investors, regulators and global reporting frameworks now require greater transparency on how capital is aligned with climate goals.

This category also connects climate performance with financial risk. High-carbon investments may carry transition risks, regulatory exposure or stranded asset risks in a low-carbon economy.

How companies estimate these emissions

Estimating Category 15 emissions involves several structured steps:

- Identifying all relevant investment and financing activities

- Determining the reporting boundary, including equity investments, debt instruments and project finance

- Gathering emissions data from investee companies

- Allocating emissions based on ownership share, enterprise value, or proportion of total financing

- Using sector-based estimates or models when direct emissions data is unavailable

In many cases, companies rely on portfolio carbon accounting methodologies and industry guidance to ensure consistency.

Challenges in reporting

Category 15 can be complex due to:

- Limited availability of emissions data from private companies

- Differences in reporting methodologies across portfolio companies

- Risk of double counting across financial institutions

- Data gaps in emerging markets

As disclosure requirements evolve, data quality is gradually improving, but estimation remains common in early reporting stages.

Strategic implications

Category 15 transforms climate reporting from an operational exercise into a strategic financial decision.

Organisations can reduce financed emissions by:

- Shifting capital toward low-carbon sectors

- Setting portfolio decarbonisation targets

- Engaging investee companies on transition planning

- Integrating climate criteria into lending and investment decisions

This category reinforces a powerful reality: capital flows shape the future economy.

The strategic perspective

Climate responsibility does not end at the factory gate or within the supply chain. It extends into financial influence.

By understanding and actively managing Category 15 emissions, organisations move from passive reporting to active climate leadership. The true carbon footprint of a company is not defined only by what it produces, but by what it chooses to support, finance and scale.

Leave a Comment